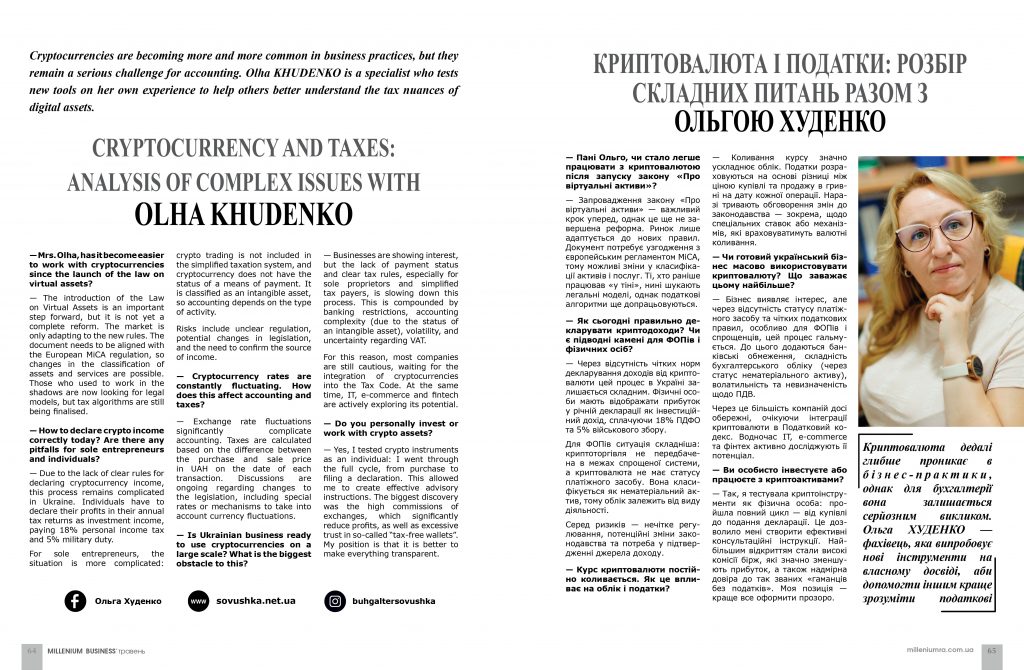

Криптовалюта дедалі глибше проникає в бізнес-практики, однак для бухгалтерії вона залишається серйозним викликом. Ольга ХУДЕНКО — фахівець, яка випробовує нові інструменти на власному досвіді, аби допомогти іншим краще зрозуміти податкові нюанси цифрових активів.

— Пані Ольго, чи стало легше працювати з криптовалютою після запуску закону «Про віртуальні активи»?

— Запровадження закону «Про віртуальні активи» — важливий крок уперед, однак це ще не завершена реформа. Ринок лише адаптується до нових правил. Документ потребує узгодження з європейським регламентом MiCA, тому можливі зміни у класифікації активів і послуг. Ті, хто раніше працював «у тіні», нині шукають легальні моделі, однак податкові алгоритми ще допрацьовуються.

— Як сьогодні правильно декларувати криптодоходи? Чи є підводні камені для ФОПів і фізичних осіб?

— Через відсутність чітких норм декларування доходів від криптовалюти цей процес в Україні залишається складним. Фізичні особи мають відображати прибуток у річній декларації як інвестиційний дохід, сплачуючи 18% ПДФО та 5% військового збору.

Для ФОПів ситуація складніша: криптоторгівля не передбачена в межах спрощеної системи, а криптовалюта не має статусу платіжного засобу. Вона класифікується як нематеріальний актив, тому облік залежить від виду діяльності.

Серед ризиків — нечітке регулювання, потенційні зміни законодавства та потреба у підтвердженні джерела доходу.

— Курс криптовалюти постійно коливається. Як це впливає на облік і податки?

— Коливання курсу значно ускладнює облік. Податки розраховуються на основі різниці між ціною купівлі та продажу в гривні на дату кожної операції. Наразі тривають обговорення змін до законодавства — зокрема, щодо спеціальних ставок або механізмів, які враховуватимуть валютні коливання.

— Чи готовий український бізнес масово використовувати криптовалюту? Що заважає цьому найбільше?

— Бізнес виявляє інтерес, але через відсутність статусу платіжного засобу та чітких податкових правил, особливо для ФОПів і спрощенців, цей процес гальмується. До цього додаються банківські обмеження, складність бухгалтерського обліку (через статус нематеріального активу), волатильність та невизначеність щодо ПДВ.

Через це більшість компаній досі обережні, очікуючи інтеграції криптовалюти в Податковий кодекс. Водночас IT, e-commerce та фінтех активно досліджують її потенціал.

— Ви особисто інвестуєте або працюєте з криптоактивами?

— Так, я тестувала криптоінструменти як фізична особа: пройшла повний цикл — від купівлі до подання декларації. Це дозволило мені створити ефективні консультаційні інструкції. Найбільшим відкриттям стали високі комісії бірж, які значно зменшують прибуток, а також надмірна довіра до так званих «гаманців без податків». Моя позиція — краще все оформити прозоро.

CRYPTOCURRENCY AND TAXES: ANALYSIS OF COMPLEX ISSUES WITH OLHA KHUDENKO

Cryptocurrencies are becoming more and more common in business practices, but they remain a serious challenge for accounting. Olha KHUDENKO is a specialist who tests new tools on her own experience to help others better understand the tax nuances of digital assets.

— Mrs. Olha, has it become easier to work with cryptocurrencies since the launch of the law on virtual assets?

— The introduction of the Law on Virtual Assets is an important step forward, but it is not yet a complete reform. The market is only adapting to the new rules. The document needs to be aligned with the European MiCA regulation, so changes in the classification of assets and services are possible. Those who used to work in the shadows are now looking for legal models, but tax algorithms are still being finalised.

— How to declare crypto income correctly today? Are there any pitfalls for sole entrepreneurs and individuals?

— Due to the lack of clear rules for declaring cryptocurrency income, this process remains complicated in Ukraine. Individuals have to declare their profits in their annual tax returns as investment income, paying 18% personal income tax and 5% military duty.

For sole entrepreneurs, the situation is more complicated: crypto trading is not included in the simplified taxation system, and cryptocurrency does not have the status of a means of payment. It is classified as an intangible asset, so accounting depends on the type of activity.

Risks include unclear regulation, potential changes in legislation, and the need to confirm the source of income.

— Cryptocurrency rates are constantly fluctuating. How does this affect accounting and taxes?

— Exchange rate fluctuations significantly complicate accounting. Taxes are calculated based on the difference between the purchase and sale price in UAH on the date of each transaction. Discussions are ongoing regarding changes to the legislation, including special rates or mechanisms to take into account currency fluctuations.

— Is Ukrainian business ready to use cryptocurrencies on a large scale? What is the biggest obstacle to this?

— Businesses are showing interest, but the lack of payment status and clear tax rules, especially for sole proprietors and simplified tax payers, is slowing down this process. This is compounded by banking restrictions, accounting complexity (due to the status of an intangible asset), volatility, and uncertainty regarding VAT.

For this reason, most companies are still cautious, waiting for the integration of cryptocurrencies into the Tax Code. At the same time, IT, e-commerce and fintech are actively exploring its potential.

— Do you personally invest or work with crypto assets?

— Yes, I tested crypto instruments as an individual: I went through the full cycle, from purchase to filing a declaration. This allowed me to create effective advisory instructions. The biggest discovery was the high commissions of exchanges, which significantly reduce profits, as well as excessive trust in so-called “tax-free wallets”. My position is that it is better to make everything transparent.